March 13, 2026

13 min read

How to write a check

Even in a digital‑first world, there are still moments when a paper check is the simplest or most secure way to pay. Chris Starr, head of deposits at Wells Fargo, walks step by step through how to write a check confidently and safely.

Key takeaways

- Writing a check is still sometimes needed for everyday payments like rent, deposits, refunds, and paying individuals.

- Always confirm your available balance before writing a check to avoid overdrafts.

- Every check follows the same steps: date, payee, amount in numbers, amount in words, memo, and signature.

- Clear writing and simple fraud prevention habits help keep checks secure.

- Tracking written checks and reconciling your account regularly helps maintain an accurate balance and spot fraud early.

At a glance: How to write a check

- Date the check on the top right.

- Write the payee’s name clearly on the “Pay to the order of” line.

- Enter the amount in numbers in the amount box.

- Write the amount in words on the line below.

- Add a memo (optional but helpful for records).

- Sign the check in the bottom right corner.

“When the information is clear and complete, you lower the chance of errors and keep the process running smoothly.”

Check writing still matters. People often write a check when giving a birthday or graduation gift or reimbursing someone. Landlords, service providers, and organizations like PTAs may prefer checks for easier bookkeeping.

“People are often surprised by how frequently checks are still needed these days,” said Chris Starr, head of Wells Fargo Deposits. “And if you’re new to banking or new to the United States, knowing how to fill out a check properly helps you avoid the common mistakes we see and protect yourself from fraud.”

This guide walks you through examples for how to write a check step by step, including how to write it to more than one person, where to sign, how to date it, and even how to void a check if you make a mistake.

Before you write the check, make sure you have enough money

Your available balance is the most up‑to‑date record of the money you can use or withdraw. It changes throughout the day as you spend, withdraw, or deposit money, or as transactions are authorized. Knowing your balance helps you avoid overdrawing your account and ensures the check can be processed without issues. To keep your balance accurate day‑to‑day, explore our tips on managing your money effectively.

Learn more about how to balance your account after writing a check.

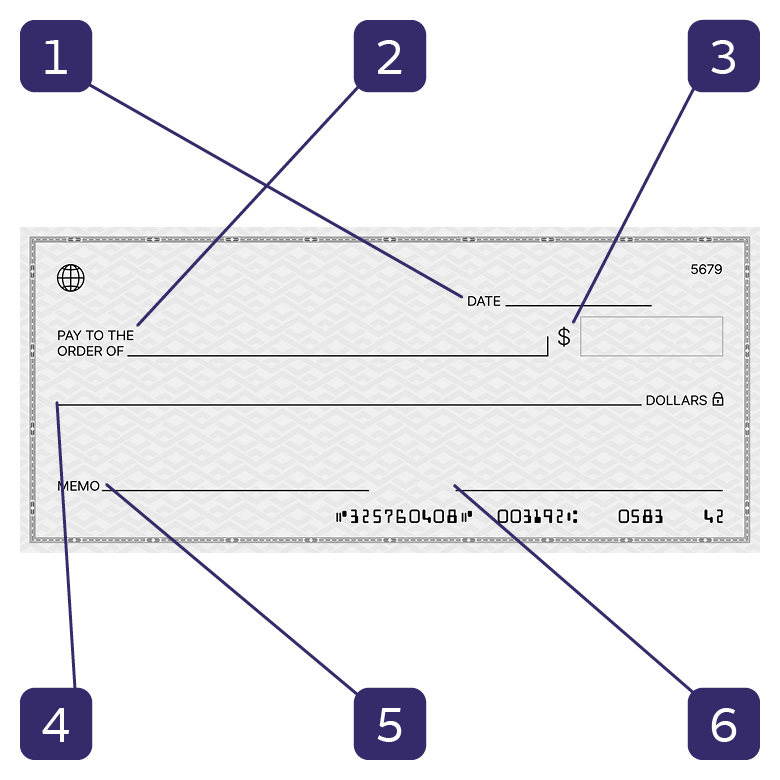

Steps to writing a check

Once you know what each part of a check represents, filling it out becomes a snap. “A well-written check is really about giving yourself a little protection,” said Starr. “When the information is clear and complete, you lower the chance of errors and keep the process running smoothly.”

Here is everything you need to do:

1. Date the check

Why dating the check matters

Checks are payable on demand, meaning they become negotiable as soon as they’re written. Because of this, the date helps the bank and the recipient confirm when the check was issued (meaning, when you wrote it), helping with accurate processing and record‑keeping.

If you’re unsure about timing, wait until the day you want the check to be cashed before writing it. Don’t leave it blank.

It’s important to know that checks generally cannot be postdated (written with a date in the future). Even if you write it for a future date, a financial institution may still process the check before that date. We’re not responsible for waiting to honor the check unless you use a stop payment order for the check. You’re responsible for notifying us to cancel the stop payment order when you’re ready to have that check paid.

How to write the date on a check correctly

- Write the date clearly on the dedicated line or box in the upper right corner of the check.

- Use today’s date in the U.S. format: Month, Day, Year (January 1, 2026) or numerical format (01/01/2026).

- Keep in mind that some fraud experts recommend writing out the month, which can make it harder to alter.

2. Write the payee’s name

In the “Pay to the order of” section, write the full legal name of the person or company. Write clearly and avoid abbreviations to ensure that the check can be deposited without delays.

You can make a check out to two people, such as a recently married couple, but keep in mind the wording determines how it can be deposited:

- If you write “Person A and Person B,” both people must endorse and deposit the check.

- If you write “Person A or Person B,” either person can endorse and deposit it.

For details on endorsement options and how signatures work when a check is made out to more than one person, see our guide on how to endorse a check.

Should you ever write a check to “Cash”?

Although not widely seen today, people used to write out a check to “Cash” (literally writing “Cash” on the payee line) when they needed money quickly and didn’t know who the payee should be. Today, this practice comes with significant risk. If the check is lost or stolen, anyone can cash it.

Alternatively, it is safer to write the check to yourself, by writing your name in the “Pay to the order of” line. Or you can use your debit card for cash withdrawals.

Learn how to prevent check fraud and scams.

3. Write the amount in numbers

When you fill in the amount on a check, the bank relies on this number to know exactly how much to withdraw from your account. Writing it clearly and in the correct format helps ensure your check is processed accurately and reduces the risk of fraud.

Write the amount in U.S. numeral format (for example, $130.45) on the line or box on the right side of the check. Even when paying a whole‑dollar amount, write out the cents, such as $410.00. Fill the space or draw a line so there’s no room for someone to add extra numbers or zeros.

Clear penmanship matters: Banks use OCR (optical character recognition) to read checks, so well‑formed numerals reduce the likelihood of processing errors.

Never hand someone a check with the amount box left blank. Once you give up control of the check, anyone could fill in a different number.

4. Spell out the amount in words

After writing the number amount in the box, you’ll also need to write the amount in words. This serves as an important accuracy check for the correct payment total: If the two amounts ever differ, the written‑out amount is the one the bank considers legally binding, according to the Consumer Financial Protection Bureau.

- Write the same dollar amount in words as it appears in the numeric box, followed by the cents written as a fraction. For example, $130.45 becomes “one hundred thirty and 45/100.”

- Even if the amount is a whole number, include the cents as “00/100” (“four hundred ten and 00/100” for $410.00).

- For clarity, use the word “and” only once, between the dollar and cents figures. Example: “One Hundred Thirty and 45/100,” not “One Hundred and Thirty and 45/100.”

- The word “dollars” is already printed on the check, so you don’t need to repeat it.

To protect against alterations, begin writing at the far left of the line and write all the way across. If any space remains at the end, draw a horizontal line to prevent someone from adding extra words or numbers. This quick step helps reduce the risk of fraud and keeps your check secure.

Being precise ensures the bank processes the correct amount and minimizes the chance of delays or disputes.

5. Add a memo

You don’t have to put anything on the memo line located in the lower left corner of the check, but it can be helpful for record‑keeping, budgeting, and avoiding confusion later. Here, you can note the purpose of the payment, such as “rent,” “electric bill,” “house cleaning,” or “PTA dues,” which can be useful when you review scanned check images in online or mobile banking for budgeting or during tax season. For more tips, explore our guide to budgeting basics to help organize your finances.

Businesses or government agencies may also ask you to include additional information, like an account number, invoice number, or phone number, to ensure your payment is applied correctly.

While the memo field is a useful reference for you and the recipient, it’s important to know that banks are not obligated to follow any restrictions or instructions, such as “void after 30 days,” “void over $50,” or “payment in full.” Banks may still process a check even if it includes such notations, is past the date you wrote, or has no date at all. Additionally, checks are paid based on U.S. dollar amounts, even if you write a foreign currency or note another instruction on the front.

In short: the memo line is a helpful personal reminder and organizational tool, but it does not serve as a binding instruction to the bank. Use it to keep your records clear but avoid relying on it to control how your check is processed.

Learn more about paying bills online.

6. Sign the check

The final step is to sign your name on the check, and it’s one of the most important. A check cannot be deposited or cashed without your signature, and your signature is what authorizes the bank to release the stated funds to the recipient. The bottom right corner is where to sign the check.

Use the same signature the bank has on file from when you opened your account. This consistency helps the bank verify that the check is legitimate. Take a moment to sign clearly. Illegible or overly stylized signatures can be easier to forge and may slow down processing.

A clean, consistent signature not only confirms your authorization but also helps protect you from fraud. Once the signature is in place, your check is complete and ready to be given to the person or business you’re paying.

How to balance a checkbook after writing a check

After you write a check, it’s important to keep your records up to date so you always know how much money is available in your account. Balancing your account helps you avoid overdrafts, track outstanding checks, and spot potential fraud or errors.

Start by recording the check in your checkbook register, budgeting app, or spreadsheet. Include the check number, the date, the payee, the amount, and your new running balance. So your records stay accurate, repeat this step for every transaction: checks you write, debit card purchases, ATM withdrawals, deposits, and fees. Wells Fargo customers can also use My Money Map tools to track spending.

Each month, compare your check register or tracking method to your bank statement. Look for differences such as checks that haven’t cleared yet, deposits that haven’t posted, or fees you may have overlooked. This is the time where you can spot any fraud on your account. When all transactions match and your adjusted balance aligns with the bank’s, your account is reconciled.

Even with online and mobile banking or if you don’t write checks often, keeping tabs on your checking account still matters. A check you wrote but hasn’t been cashed won’t show in your online balance, but it will appear in your register. Maintaining your own record gives you a more accurate picture of your spending, helps you avoid overdraft fees, and provides an extra layer of protection against fraud. If you believe there is an error on your bank statement, contact your bank as soon as possible. Wells Fargo customers can call 1-800-869-3557.

Fraud prevention and security tips

Checks may feel pretty basic, but they also give someone direct access to money in your account once deposited. “Fraudsters look for small openings, so the way you handle a check matters,” Starr said. “Using gel ink, securing your checkbook, and reviewing your account regularly can make a big difference in keeping your money safe.”

Here are a few precautions that can help keep your payments secure and protect you from fraud.

What is check fraud?

Fraudsters use the following methods to manipulate checks, which they present to a bank to be cashed or deposited into their own accounts.

-

Check theft: Thieves acquire checks through normal day-to-day commerce, by stealing them out of personal and U.S. Postal Service mailboxes or even obtaining customer account and routing numbers through phishing scams. They endorse the checks or make a copy with their own information on it.

-

Check washing: Criminals use chemicals to “wash” or erase the original ink on the check to then change the amount and/or payee.

-

Check forging: Criminals create fake or counterfeit checks using legitimate routing and account information.

The Financial Crimes Enforcement Network has issued alerts warning that mail theft and check washing have risen sharply in recent years. Learn more about protecting yourself from check fraud and scams.

How to reduce your risk

- Use black or blue gel ink, which is harder to alter.

- Fill in unused spaces on the amount line or box so no one can add numbers or words.

- Keep your checks in a secure place, and shred old or voided checks.

- Avoid mailing checks from home mailboxes. Drop them inside a post office when possible.

- Consider using Bill Pay, Zelle®1, or other digital payment options that offer stronger protections.

- Turn on account alerts so you’re notified when transactions post.

- Regularly review bank statements and check images to spot unauthorized changes early.

How to avoid check scams

Fraudsters often try to trick people into depositing a bogus check and sending money back. In fact, the Federal Trade Commission highlights fake check scams as one of the most common forms of fraud and offers guidance on warning signs. These scams may appear in the form of overpayment offers, sweepstakes “winnings,” fake job sign‑on bonuses, or requests from someone pretending to be a friend, family member, or law‑enforcement official.

To protect yourself:

- Never accept or cash a check for more than you expected to receive.

- Don’t send money back to someone who paid you with a check.

- Don’t share your account or routing numbers with anyone you don’t know and trust.

- Be cautious with unsolicited offers, pressure tactics, or instructions that feel unusual.

If you ever spot something suspicious, such as an altered check image or a withdrawal you don’t recognize, contact your bank right away. Wells Fargo customers can call 1‑800‑869‑3557.

Read more about protecting yourself from check fraud and scams.

Top mistakes when writing a check

Starr said the most avoidable mistake people make is leaving room for confusion. “An amount that’s not fully written out or extra space on a line might not seem like a big deal in the moment, but that’s where errors or fraud can happen,” he said. “A check should always be filled out completely, clearly, and in one sitting.”

Common check-writing mistakes include:

- Mismatching the dollar and cents amounts with the spelled-out amount.

- Writing the date incorrectly or forgetting it.

- Misspelling the payee’s name.

- Leaving extra space in the amount box or words line.

- Forgetting to sign the check.

- Using pencil or ink that can be altered.

FAQs

Write the amount using U.S. numerals in the amount box (for example, $236.79). Then spell it out on the amount‑in‑words line as “two hundred thirty‑six and 79/100.” For whole‑dollar amounts, write “00/100” for clarity.

Sign your check in the bottom right corner using the same signature the bank has on file.

Void the check by writing “VOID” in large letters across it and start a new one. Shred the voided check for security.

Most personal checks are considered stale‑dated if they aren’t cashed within six months (180 days) of when they were written. Banks may decline them or return them as non‑negotiable. For government‑issued Treasury checks, the IRS notes that they typically expire after one year.

Write “VOID” in large letters across the front or write “VOID” on each line individually. Record the voided check number in your check register. Finally, if you use duplicate checks, make sure your “VOID” marks are seen on the duplicate, too. For extra security, shred the voided check.

Use mobile deposit in your bank’s app, deposit at an ATM, or visit a branch. (Read more about Wells Fargo Mobile® Deposit.)

Writing a check to yourself is one way to move money between your accounts or to an account you have at another bank, and it creates a paper record of the transfer.

People still write checks for several reasons, especially when a payment needs a clear paper trail or the recipient doesn’t use digital payment tools. Typical situations include paying rent, reimbursing friends or family, giving gifts (such as for a birthday, wedding, or graduation), or paying individuals for services like house cleaning, repairs, child care, or tutoring. Checks are also used for deposits, refunds, and situations where someone prefers not to share their phone number or digital payment details.

Banks may process a check before the future date you write, so it’s best to wait until the funds are available in your account.

No, you typically can’t write checks from a savings account. Savings accounts usually don’t offer check-writing privileges. Learn more about the differences between checking and savings accounts.

Sign your name, then write “Pay to the order of” and the person’s name you want to sign the check over to. (See How to endorse a check.)

- Routing number identifies your checking account’s financial institution.

- Account number identifies your specific checking account.

- Check number helps you and the bank track individual checks.

Read more in What are routing and account numbers.

Yes. If you make the check out to two people, how you list their names determines who must endorse it. “A and B” means both must sign, while “A or B” allows either one to sign and deposit it.

A check “bounces” when you write a check but there isn’t enough money in your account to cover it. The check is returned to the recipient unpaid, and you may get charged a fee.

If you ever notice an unauthorized transaction, an altered check image, or anything unusual, contact your bank right away. Wells Fargo customers can call 1‑800‑869‑3557.

Want help with basic banking skills?

A Wells Fargo banker can walk you through the steps and answer any questions.