March 12, 2026

What are routing and account numbers?

Have you ever wondered how your direct deposit so seamlessly is deposited into your account? You can thank your routing and account numbers for that. Chris Starr, head of deposits at Wells Fargo, shares what you need to know to successfully send and receive money with transfers.

Key takeaways

- A routing number is a nine-digit code that identifies your bank.

- A bank account number identifies your specific account where funds are deposited or withdrawn.

- Routing numbers support transfers including direct deposit, ACH payments, and domestic wires.

- Banks may use different routing numbers by state or transaction type.

According to PayrollOrg, 92% of U.S. workers now receive their wages through direct deposit (2024). The federal government also completed its transition to fully electronic payroll in 2025.

So, chances are, if you’ve recently set up direct deposit, started a new job, or are waiting for a tax refund, you’re familiar with the two numbers that make these financial transactions possible:

- Your individual bank account number

- Your bank’s routing number

Understanding how these numbers work helps ensure your money is where it’s supposed to be, when you need it to be.

Your bank’s routing number is sometimes also called a routing transit number (RTN) or an Automated Clearing House (ACH) routing number, depending on the type of transaction. These terms all refer to the numbers that help identify where your money needs to go.

“Direct deposit is the industry and government standard because it gives reliability and peace of mind,” Chris Starr, head of deposits at Wells Fargo, said. “Your account and routing numbers are key to making that happen. When people fully understand what these numbers do, they understand the importance of knowing them and keeping them safe and secure.”

What is a bank account number?

Your bank account number identifies your specific account where funds are deposited or withdrawn.

What is a routing number?

A routing number, sometimes called an ABA number, is a unique identifier that directs electronic payments to the correct financial institution. Routing numbers also embed Federal Reserve processing information. The first few digits indicate the Federal Reserve district and processing center.

How routing numbers are used

Routing numbers are used for a variety of everyday financial transactions, including:

- Receiving IRS refunds or making federal tax payments

- Direct deposit for payroll or government benefits

- Autopay for utilities, rent, and subscriptions

- Loan, insurance, and credit card payments

- Bank-to-bank transfers

- Domestic wire transfers

- Mobile check deposits

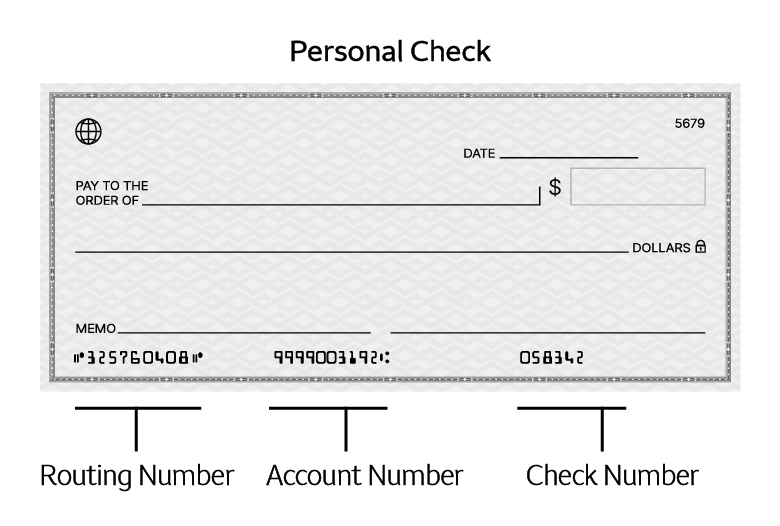

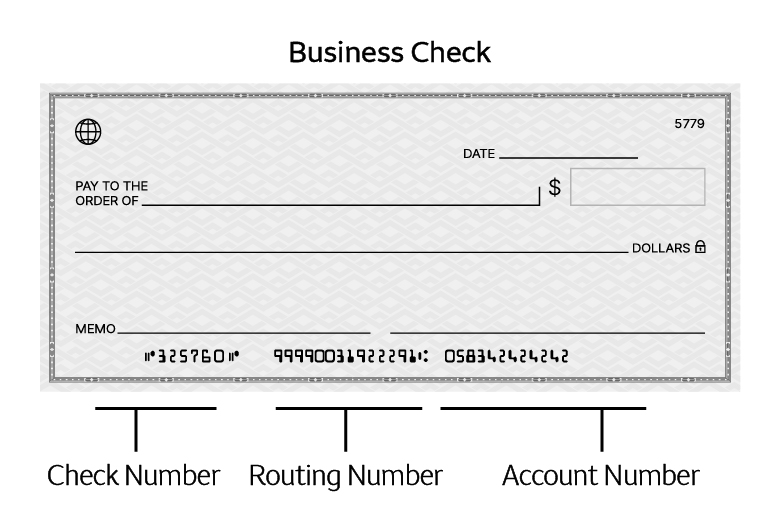

Where to find your routing and account numbers

Knowing where to find these numbers — and which one to use for ACH, wires, or checks — ensures your payments are delivered quickly and accurately.

For personal checks, your routing number typically appears at the bottom left of the check. Your account number appears just to the right. Routing numbers for most banks and credit unions are available online or through mobile apps. Account and routing numbers for Wells Fargo customers are available online.

Other ways to find your numbers:

- Account statements

- Customer service

ACH payments and timing

ACH is an electronic money transfer made between banks and credit unions across a network called the Automated Clearing House (ACH), and these transactions use your routing number and account number to complete electronic transactions.

In 2021, Federal Reserve data showed that ACH usage has grown steadily, with 34.2 billion ACH transfers in that year alone. Wire transfers are a fast and easy way to send money from your account to individuals or businesses.

“The ACH network is a secure, fast, and an efficient way to transfer funds,” Starr said. “It allows millions of transactions to clear, on time, each day. Reliability is one of its greatest strengths, giving consumers and businesses peace of mind.”

ACH is used for:

- Direct deposit

- Recurring bill payments

- Online banking payments

- Person-to-person transfers

ACH payments can clear the same day, but they often take 1–3 business days depending on bank cutoff times and fraud prevention safeguards. They may be returned (“bounce”) if there isn’t enough money in the account.

International transfers

Routing numbers are only used for domestic transfers in the United States. International transfers typically require a SWIFT/BIC code. Wells Fargo customers can find these details in the Transfers & Wires section of Wells Fargo Online® or Wells Fargo Mobile®.

Why banks have multiple routing numbers

Most banks and financial institutions have multiple routing numbers due to one of three factors:

- Federal Reserve processing regions

- Mergers and acquisitions

- Separate numbers for different transaction types (Wires, checks, ACH)

The first two digits of a routing number identify the Federal Reserve district where the bank is located. Since many banks and financial institutions operate in various regions throughout the country, they may have different routing numbers used in different Federal Reserve processing zones.

The Federal Reserve assigns routing numbers through ABA processes and says that routing numbers can remain tied to specific banks or “payable-through” institutions, even when operations change.

Banks may have one routing number for ACH, one for wires, and one shown on paper checks, because each transaction type uses different Federal Reserve networks (FedACH, Fedwire, and check clearing).

Many banks, including Wells Fargo, use more than one routing number depending on the type of transaction:

- ACH routing number: Used for direct deposits, online bill payments, and other transfers.

- Wire routing number: Used specifically for domestic wire transfers.

- Check routing number: Printed on the bottom of paper checks.

Your routing number may vary depending on the state where your account was opened or the type of transaction you’re completing.

Safely sharing routing and account numbers

Sharing your routing and account numbers is generally safe when you’re setting up direct deposit, paying bills, or authorizing trusted and verified companies to withdraw from your account.

You should only provide these numbers to known, trusted, and verified parties. Monitoring your account for unauthorized debits is one way to avoid scammers. If your account and routing numbers are compromised, alert your bank or credit union immediately.

Because wire transfer payments are typically irreversible, they are commonly used in scams. Check out these five tips to avoid wire transfer scams.

For more information, resources, and tips on spotting and avoiding scams, visit the Wells Fargo Security Center.

FAQ

The difference between routing numbers and account numbers is simple — routing numbers identify your bank, and account numbers identify your specific account.

The payment may fail, be delayed, or returned by the receiving bank.

Routing numbers can vary by state, region, or transaction type.

Usually, direct deposits don’t arrive for one of three reasons:

- An ACH delay or return

- The deposit was submitted after cutoff times

- The routing or account number was incorrect

You can find your routing number at the bottom left of your personal check. The location could differ on a business check.

Your bank account number can be found on your check, or likely on your bank or credit union’s website. Wells Fargo customers can find their bank account number here.

An ABA number is the routing number, but some banks use different routing numbers for ACH transfers. However, both identify the same bank.

A routing number is always nine digits.

No, you do not need a routing number for international wires. International wires usually require a SWIFT/BIC code.

Yes, it is safe to share your routing and account numbers with trusted, verified parties for deposits or payments. You should only share account and routing numbers when strictly necessary and only with organizations you have independently verified. Never share them by email or text. Monitor your accounts and set up alerts. If you suspect misuse, contact us immediately.

Growing your financial health toolbox is a good thing.

Swing by your local Wells Fargo branch, where a banker can walk you through all things related to account numbers, ABA numbers, and ACH payments.