September 16, 2025

14 min read

Raise money-smart kids: How to teach financial literacy at home through the magic of allowances

An allowance isn’t just pocket money — it’s a way to spark important money talks and life lessons.

Key takeaways

- Allowances are a powerful tool for introducing financial education at home, helping kids learn how to save, spend, and make decisions.

- Discuss what it means to have good money habits — and practice what you preach.

- Consider using digital tools like Zelle®1 and direct deposits to teach modern money management.

- It’s important to find a balance between supervising your kids and allowing them to make their own mistakes.

- Be mindful of how inflation can influence your family’s financial behaviors and assess adjusting allowances accordingly.

If you got an allowance when you were a kid, did you realize you were getting more than just spending money in your pocket? You were actually getting a crash course in financial responsibility.

It turns out 71% of today’s parents are on the same page with giving their kids an allowance, according to the 2025 Family Banking and Allowance Study by Wells Fargo.

“Children today have different financial experiences than their parents did,” said Louann Millar, leader of youth and student banking at Wells Fargo. “We have an opportunity, and a responsibility, to provide support, guidance, and tools to help parents set their kids up for success with money.”

Good money habits start with a chat

“Whether you’re giving your child $5 or $35 a week, the payment opens the door to a financial conversation,” she said. “You can explain what a dollar can buy and how budgeting for tomorrow begins today, while giving your children the ability to manage their own money with online and mobile banking tools.”

While 85% of parents want to have more conversations with their kids about good money habits, more than half of parents struggle to talk about money in a way their kids will understand, according to the study. “A lot feel they aren’t fully equipped,” said Millar. “I’ve heard of adults who don’t think they have the best money habits and feel like they have imposter syndrome when teaching their kids about money.”

The good news is you both can benefit from learning together. “The weekly activity of giving the allowance presents an opportunity for parents to discuss needs versus wants with their children. It’s an opportunity to discuss your own money habits and prioritization,” Millar said. Don’t be scared to share your own mistakes. These early conversations are great money lessons for kids — and they’ll help you feel more confident about how to teach kids about money, too.

Find teachable moments. It can be difficult to find time to sit down and talk specifically about finances, but natural opportunities to teach pop up every day. For younger kids, a trip to the grocery store could include a discussion about wants versus needs. For older kids, show them how to be smart consumers by comparing prices, looking for deals, and making informed purchasing decisions.

Talk to your kids about what they spent their allowance on and how it made them feel. Consider these value-based conversation starters: What matters in our family? How do we feel about our family? What could we do to help someone else, such as philanthropy or charitable events? If someone is responding with a lot of questions, go where the energy is; maybe they will be the early adopter for financial literacy.

Introduce mindful spending. Encourage them to consider the value and necessity of each purchase and to prioritize their needs over wants. Discuss the joy of immediate rewards like toys, candy, or gaming power-ups. Conversely, help them envision larger purchases such as electronics, a new bike, or even a car as part of their long-term dreams. Help your child set and work toward saving for a specific item they want, demonstrating delayed gratification. This is a great way to show how to save money as a kid while still enjoying small rewards.

Read more

Beyond apps: Why your teenager needs a bank account

With so many payment apps available today, some teens may consider skipping out on a bank account. Here’s what they could be missing.

Teaching your children about money

How can you help build money skills and promote good habits?

7 smart things to do with your summer job and side hustle money

It’s your money. You earned it. Here’s how to spend it.

When it comes to teaching kids about money, it’s important to remember two things: Start early, and know that there isn’t a one-size-fits-all approach.

Starting financial conversations with your family

Waiting for the perfect time to have important financial conversations with your children? Maybe it’s now.

Build financial fluency and independence. Your goal is to raise a child who is fluent in money and independent. Think about the first time you saved up to buy something or made an impulse buy that you regretted, then the second time and then the third. Each time you go through that process, you become more fluent. You understand the pros and cons of using your money.

Independence is about being able to confidently navigate money decisions without any help from a family member. This doesn’t mean you don’t rely on others. Instead, you can live on your own and manage your own financial situation. This may seem a long way off from where your child is now, but it’s a goal.

Test and learn. Revise as your kids grow older. High school students should know where their money goes each month so they can prepare for when they are out of the house and on their own. One option to explore is setting your teen up with a debit card so they can learn to manage the funds in their bank account. Banking apps, like the Wells Fargo Mobile® App, give them a quick view of how much they have available and how much they’ve spent. And keep in mind, what works for one of your kids may not work for the other.

Practice what you preach. Kids are smart enough to pick up on whether parents follow the same rules that they set for their children. If you want your children to save some of their money and give back to the community, you should do the same. As your children get older, you can help them track expenses. Modeling responsible financial behaviors is a good way to teach your kids about money.

Set a schedule

How often should kids receive an allowance: weekly or monthly? Each frequency has its own benefits and can be tailored to fit different needs and circumstances. Ultimately, the cadence depends on your child’s age, maturity, and financial understanding, as well as your preferences and goals. Don’t be afraid to test and learn together.

If you’re wondering what age to give an allowance or how much allowance to give, consider your child’s maturity and financial understanding. The right schedule depends on what works best for your family. Here are some ways to think about it:

Weekly

- Helps kids learn to manage money on a short-term basis, which can be beneficial for younger children who are just starting to understand financial concepts.

- Requires more frequent monitoring and adjustments, so it may be good if you prefer regular check-ins and discussions about money management. As time goes by, consider stretching to bi-weekly.

Monthly

- Encourages long-term planning and saving. It can be a good choice for older children who are ready to handle larger sums of money and make more significant financial decisions.

- Requires a higher level of responsibility and self-control. It may be suitable for families who want to foster independence.

-

![A young boy washes dishes while scowling at the camera]()

Allowance is more than just pocket money. It’s a chance to teach smart spending habits.

-

![Two students smile as they look at a smartphone]()

70% of parents say kids should learn to use digital tools like Zelle® and mobile banking.

Source: Wells Fargo 2025 Family Banking and Allowance Study -

![A father and son smile at each other]()

Whether it’s $5 or $35 a week, the real value is in the conversation.

What's the best way to give allowance?

“The most surprising result of this study is how much cash is being used, even as parents understand their children prefer digital payment options,” Millar said. With cash, you’ve got that tangible feeling of running out. “When it’s gone, it’s gone. Some adults I know take out cash at the beginning of the week for fun money — that’s their guardrails,” she said. But it also can be easy to lose — in the bottom of backpacks, on a bus seat, in the washing machine, and so on.

The majority (70%) of parents in the study believe that teaching kids about money today should emphasize digital tools, such as peer-to-peer (P2P) payments like Zelle® and direct deposits or transfers to bank accounts. And not surprisingly, teens aged 15 to 17 years are more likely to receive allowance through P2P (34%) compared to younger kids.

As you share your knowledge on how to use these tools, you can discuss with your child ways to avoid online payment scams. For example, explain that you shouldn’t use Zelle® unless you know and trust the recipient, because once you authorize a payment to be sent, it can only be canceled if the recipient has not yet enrolled with Zelle®. And do not share your private account access information, so scammers can’t send or receive online payments without your permission. Read more about online payment scams.

Balancing supervision and independence

How much guidance should you give your child? According to the study, 65% of parents find it hard to let their kids make money mistakes, even though over 75% trust their kids to make good choices. Almost all parents in the study understand that early success with money starts with small, supervised choices. Choosing an account with guardrails allows you to have visibility without being a helicopter mom or dad. It’s important to find a balance, allowing your kids to learn from their mistakes while still providing the necessary support and guidance.

When choosing a bank account for your child, consider options like Wells Fargo’s Clear Access Banking account. Key features include mobile deposit,2 bill pay, and the ability to send and receive money with Zelle®1.

Consider opening a joint savings account, such as the Wells Fargo Way2Save® Savings account, to help your kids start building smart money habits. Teens can also set up automatic transfers3 from their checking account on a daily or monthly schedule to stay consistent.

Using a bank account can give your kids a big-picture view of their deposits, savings, and spending. Some banks offer virtual assistants, like Fargo®6, to help them understand their finances even more.

Just as you ensure your child is safe on social media, it’s important to check on their finances. With joint ownership or authorization, you can monitor their bank account for fraudulent or suspicious transactions, or coach them to do so. This includes checking if their information has been stolen, spotting unauthorized charges, or identifying scams where they might be tricked into sending someone money.

The impact of inflation

Economic pressures like inflation are influencing family financial behaviors. While 29% of parents have increased their kids’ allowances over the last year to keep up with inflation, 65% have not, and 6% have decreased the amount they give their children, according to the survey.

“It’s different for different families,” said Millar. “While one parent might say ‘I’m increasing your allowance because inflation is causing prices to rise,’ another might say ‘Inflation is impacting this family as a whole and therefore I’m going to have to decrease your allowance.’” These are money lessons for kids based on real-world economics.

Whether you’re wondering what age to give allowance or how to teach kids about money, starting early with consistent habits can lay the foundation for lifelong financial literacy. “There’s no one way to talk about money with your kids,” Millar says. “The most important thing is to just do it.”

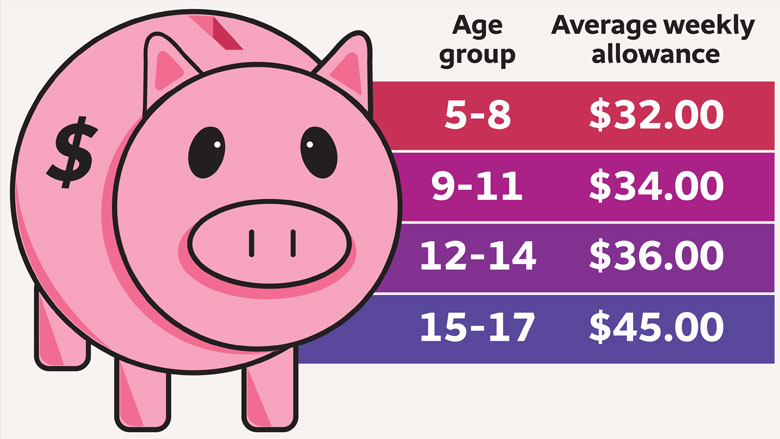

What’s the going rate?

The average weekly allowance for kids ages 5 to 17 is $37.19 in 2025, according to the survey. And allowances generally rise as kids age. But don’t sweat it too much. “Any amount is fine as long as you don’t miss this opportunity to talk about money with your child,” said Millar.

FAQ

- Not having conversations about money: You want your kids to have good money habits, but sometimes it’s hard to follow through. Make it a priority to discuss financial topics regularly.

- Not balancing supervision and independence: While you trust your kids to make good choices, it can be tough to let them make money mistakes. Set up guardrails, like a banking account with no overdraft, and talk about how to remedy mistakes, such as curbing impulse spending.

- Not reassessing for age, situation, and inflation: Make it a habit to revisit your plan often to keep up with inflation, or reassess your approach based on your child’s age and maturity level.

- Not introducing digital tools: Teaching your kids how to manage digital tools and avoid scams is becoming more important.

- Letting your own hang-ups about money get in the way: Your own anxieties and attitudes can influence how you handle allowances for your kids. Focus on teaching healthy habits and encourage open discussions. Be your own role model by demonstrating good financial behavior and showing them how to manage money wisely.

- Not setting clear expectations: Without a discussion on what the allowance is for and how it should be managed, your kids may not grasp your intended lessons. Set simple goals and guidelines to help them understand how to use their money wisely.

This is one of the most common questions parents ask when exploring financial literacy for kids. The average weekly allowance for kids ages 5 to 17 is $37.19 in 2025. Allowances generally rise as kids age. Millar advises, “Don’t miss this opportunity to talk about money with your child.”

It’s a great tool for teaching kids about money because it gives them hands-on experience managing money with your guidance, so they can learn in a safe environment. It also opens the door for conversations about needs versus wants and lets you share your own money habits along the way.

Share your values, demonstrate budgeting, and find teachable moments in everyday situations. Involve your children in creating a household budget and discuss financial concepts practically.

Teaching kids about money today should emphasize digital tools like Zelle® and direct deposits. Discuss ways to avoid online payment scams and ensure kids understand the importance of secure transactions.

About the survey

The findings are from a Wells Fargo survey, with data collection provided by Ipsos, conducted between April 28 – May 8, 2025. A sample of 1,587 U.S. parents — aged 18 and older with at least one child between 5 and 17 years of age in the household — were surveyed online in English, as part of Ipsos Omnibus shared survey program. The results of this research have a credibility interval of plus or minus 3.0 percentage points for all respondents. Respondents were asked questions about their child in one of the following age groups: 5 to 8 years of age, 9 to 11 years of age, 12 to 14 years of age, or 15 to 17 years of age. If they had more than one child, they were randomly asked about only one of the age groups.